达里奥万字长文:巨大泡沫与贫富鸿沟并存的重大风险(逐段翻译)

Author: Ray Dalio

Original link: https://mp.weixin.qq.com/s/J7OfMmj7mDgjx_uuDof7WQ

Note: All rights belong to the original author. This post includes brief excerpts for commentary and review. Please read the full article at the source.

Published on 2025-11-22

Ray Dalio 2025年11月22日 19:09

关起门来说亮话

🔷 来源:Ray Dalio《The Big Dangers of Big Bubbles with Big Wealth Gaps》 | 整理:Jevons

⭐原文发布于2025年11月21日

While I am still an active investor hooked on the investing game, at this stage in my life, I am also a teacher trying to pass along what I’ve learned about how reality works and the principles that helped me deal with it well. Since I have been a global macro investor for over 50 years, and learned a lot of lessons from history, naturally a lot of what I pass along is about that.

尽管我仍是一名活跃的投资者,沉迷于投资领域,但在人生的这个阶段,我也是一名教师,试图分享我所学到的现实运作规律及帮我妥善应对现实的原则。由于我从事全球宏观投资已逾 50 年,从历史中汲取了诸多教训,因此分享的内容自然多与此相关。

注: 现年 76岁的达里欧并未选择退休,而是接管其达里欧家办 (Dalio Family Office, DFO) 的投资事务。

This note is about:

- The important difference between wealth and money, and

- how that drives bubbles and busts, and

本文旨在探讨:

- 财富与货币的重要区别;

- 二者如何催生泡沫与崩盘;

- 这种机制在伴随巨大贫富鸿沟时,如何刺破泡沫并引发兼具金融、社会与政治动荡的崩盘。

It is important to understand the difference between wealth and money and the relationship between them, most importantly: 1) how bubbles occur when the amount of financial wealth becomes very large relative to the amount of money, and 2) how bubbles burst when there is a need for money that leads to the selling of wealth to get money.

理解财富与货币的区别及二者关系至关重要,核心两点的是:

1)当金融财富规模远超货币总量时,泡沫便会产生;

2)当人们需货币而出售财富换钱时,泡沫就会破裂。

This very basic, simple-to-understand concept about the mechanics of how things work is not well understood but has helped me a lot in my investing.

这个关于事物运作机制的基础易懂概念虽未被广泛认知,却对我的投资助力极大。

The main principles to know are that:

- Financial wealth can be created very easily and doesn’t represent its true value;

- financial wealth is of no value unless converted into money to spend;

- andconverting financial wealth into money that can be spent requires selling it (or collecting its yield), which is what typically turns bubbles into busts.

需掌握的核心原则:

- 金融财富极易创造,且不代表其真实价值;

- 金融财富除非转化为可消费货币,否则毫无价值;

- 将金融财富转为可消费货币需出售财富(或收取收益),这通常是泡沫演变为崩盘的导火索。

Regarding “financial wealth can be created very easily and doesn’t represent its true value,” for example, nowadays if a founder of a startup sells shares in a company—let’s say $50 million worth—and values the company at $1 billion, then the seller has become a billionaire. This is because the company is worth $1 billion even though there is nowhere near $1 billion behind that wealth number. Similarly, if buyers of a publicly traded stock buy a few shares from sellers at a particular price, all shares are valued at that price, so by valuing all shares at that price you can determine the amount of wealth that exists in that company. Of course, these companies might not really be worth those valuations, as assets are only worth what they can be sold for.

关于 “金融财富极易创造,且不代表其真实价值” ,例如如今某初创企业创始人出售 5000 万美元公司股份,给公司估值 10 亿美元,那他就成了亿万富翁。即便支撑该财富数字的实际资产远不足 10 亿美元,公司仍被估值 10 亿美元。同理,若上市公司股票买家以特定价格购入少量股份,所有股份均按该价估值,由此可算出公司财富规模。当然,这些公司实际价值未必匹配估值,因资产价值取决于可售价格。

Regarding “financial wealth is essentially worthless unless converted into money,” this is because wealth can’t be spent but money can.

关于 “金融财富除非转化为货币,否则本质无价值” ,原因是财富无法直接消费,而货币可以。

When there is a lot of wealth relative to the amount of money, and those with wealth need to sell it to get money, the third principle applies: “converting financial wealth into money that can be spent requires selling it (or collecting its yield), which is what typically turns bubbles into busts.”

当财富总量远超货币总量,且持有者需售富换钱时,第三条原则生效:“ 将金融财富转为可消费货币需出售财富(或收取收益),这通常是泡沫演变为崩盘的导火索。”

若能理解这些,便能知晓泡沫的形成与破裂逻辑,进而预判并应对泡沫与崩盘。

It’s also important to know that while both money and credit can be used to buy things, a) money settles the transactions, whereas credit creates debt that requires one to get money in the future to settle the transaction, and b) credit is easy to create, while money can only be created by the central bank. While one might think that one needs money to buy things, that’s not entirely true because one can buy things with credit, which creates debt that needs to be paid back. That’s typically what bubbles are made of.

同样重要的是, 货币与信贷均可购物,但:a)货币可完成交易结算,信贷会产生债务,需未来用货币偿还;b)信贷易创造,货币仅能由央行发行。人们或认为购物必用货币,实则不然,信贷购物会产生债务,这通常是泡沫的成因。

Now, let’s look at an example.接下来看一个例子。

While throughout history all bubbles and busts worked in essentially the same way, I will use the 1927-29 bubble and the 1929-33 bust as examples. If you think mechanistically about how the bubble of the late 1920s and the bust and the depression of 1929-33 worked and what President Roosevelt did to relieve the bust in March of 1933, you will see how the principles I just described worked.

纵观历史,所有泡沫与崩盘机制本质相同,以1927-1929年泡沫及1929-1933 年崩盘为例。从机制层面看20世纪20年代末泡沫、1929-1933年崩盘与大萧条,以及罗斯福总统1933年3月救市举措,便能印证上述原则。

Where did all the money come from to finance all the stock buying that made the stock market go up so much to make the bubble, and what made it a bubble? Common sense tells you that if there were a limited supply of money in existence and everything needed to be bought with money, then buying anything involves taking money out of something else. That something else probably would go down in price because of the selling, and the item being purchased would go up in price. However, it wasn’t money—it was credit then (e.g., in the late 1920s), always, and now, and credit can be created without money to buy stocks and other things that made the bubble. The dynamic then, which is the most classic dynamic, was that credit was created and borrowed to buy the stocks, which created debt that had to be paid back, so when the money needed to service the debt was greater than the money produced by the stocks, the financial assets had to be sold, which caused them to go down in price, and the bubble dynamic worked in reverse to make the bust dynamic.

支撑股市暴涨催生泡沫的购股资金源自何处?为何成泡沫?常识而言,若货币供应有限且购物必用货币,购一物需从他处抽钱,被抽钱资产或因抛售降价,所购资产涨价。但当时、过往及如今,支撑泡沫的是信贷而非货币,无需货币即可造信贷购股及其他资产。当时最典型机制:借信贷购股产生债务,当偿债资金超股票收益,需售金融资产,价格下跌,泡沫机制逆向转为崩盘机制。

The general principle for how these dynamics drive bubbles and busts is that:

When financial asset buying is financed by a lot of credit growth and the amount of wealth rises relative to the amount of money (so that there is a lot more wealth than there is money), that creates a bubble, and when wealth needs to be sold to get money, that creates a bust.

此类机制催生泡沫与崩盘的通用原则:

金融资产购买依赖大量信贷增长,财富规模远超货币总量时,泡沫形成;需售富换钱时,崩盘发生。

For example, in the 1929-33 period, stocks and other assets had to be sold to pay the debt service on the debts that had been used to buy them, so the bubble dynamic worked in reverse. Naturally, the more borrowing and buying of stocks, the more they did well, and the more people wanted to buy them. These buyers didn’t have to sell anything to buy them because they could buy them with credit. The more they did that, the more credit became tighter and interest rates rose, both because the demand to borrow was so strong and because the Fed let interest rates rise (i.e., it tightened monetary policy). When the borrowing needed to be paid back, the stock had to be sold to get the money to service the debt, so prices fell, debt defaults happened so collateral became worth less, the availability of credit shrank, the bubble turned into a self-reinforcing bust, and a depression followed.

例如 1929-1933 年,需售股票等资产偿还购股债务,泡沫机制逆向运转。借信贷购股越多,股价越涨,购股意愿越强,买家无需售他物即可购股。此类行为越多,信贷越紧、利率越高 —— 既因借款需求旺,也因美联储放任加息(即收紧货币政策)。借款到期需售股偿债,股价跌、违约增、抵押品贬值、信贷收缩,泡沫演变为自我强化的崩盘,随后大萧条来临。

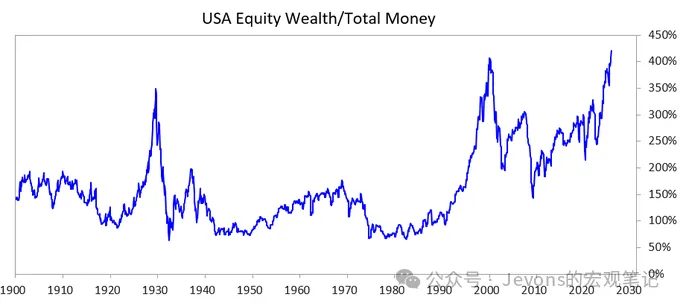

为探究该机制与贫富鸿沟并存时如何刺破泡沫、引发多领域动荡,我研究了下图。图中呈现过往及当前财富与货币差距,即股票总价值相对货币总价值的比例。

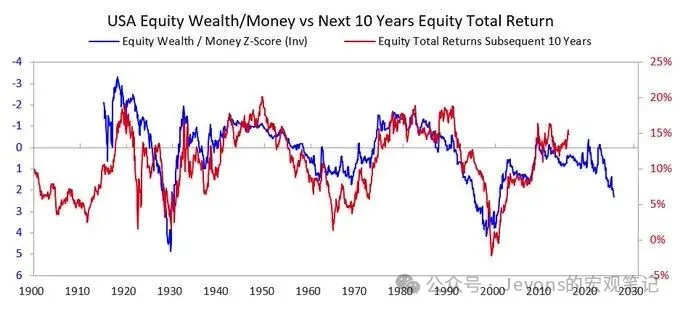

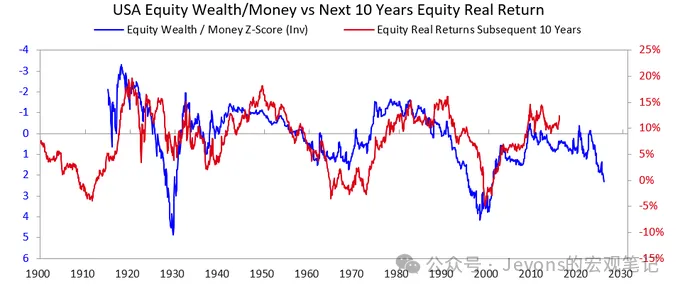

The next two charts show how that reading is an indicator of the next 10 years’ nominal and real returns. These charts speak for themselves.

接下来两张图显示该数据对未来 10 年名义与实际回报率的预示作用,图表已清晰呈现。

When I listen to people trying to assess whether a stock or the stock market is in a bubble by trying to figure out whether the companies will end up becoming profitable enough over time to provide an adequate return for the current prices, I think to myself that they don’t understand the bubble dynamic. While what an investment will earn is of course important over time, it isn’t the primary reason bubbles burst. Bubbles don’t burst because people wake up one morning and determine that there won’t be enough revenue and profits to justify the price. After all, whether or not there will be enough revenue and profits to provide a good ROI won’t be known for many years, typically decades.

当人们通过判断企业长期盈利能否支撑当前价格,评估股票或股市是否处泡沫时,我认为他们不懂泡沫机制。长期看投资收益虽重要,却非泡沫破裂主因。泡沫不会因人们突然察觉营收利润撑不起价格而破,毕竟企业能否实现良好回报率,通常需数年甚至数十年才知晓。

The principle to keep in mind is that:

Bubbles pop because the money flowing into the asset begins to dry up and the holders of stocks and/or other wealth assets need to sell them to get money for some purpose (most commonly for debt service payments).

需牢记原则:泡沫破裂因流入资产资金枯竭,股票等财富持有者为某目的(最常见为偿债)需售资产换钱。

What typically comes next?泡沫破裂后通常会怎样?

After bubbles pop, when there isn’t enough money and credit to meet financial asset holders’ needs, the markets and economy decline, and internal social and political disruptions typically increase. That is especially true if there are large wealth gaps because they intensify the differences and the anger between those of the rich/right and those of the poor/left. In the 1927-33 case that we are looking at, that dynamic caused the Great Depression that led to great internal conflict, particularly between the rich/right and the poor/left. This dynamic led to President Hoover getting thrown out of office and the election of President Roosevelt.

泡沫破裂后,若货币信贷不足支撑金融资产持有者需求,市场与经济下滑,国内社会政治动荡加剧;若有贫富鸿沟,情况更甚,会激化富裕 / 右翼与贫困 / 左翼群体的分歧与不满。1927-1933 年案例中,该机制引发大萧条,导致国内严重冲突,尤其两类群体间矛盾,进而让胡佛总统下台、罗斯福总统当选。

Naturally, when bubbles burst and there are market and economic declines, these things lead to big political changes, big deficits, and big debt monetizations. In the 1927-33 example, the market and economic declines happened in 1929-32, the political changes came in 1932, and these things led to President Roosevelt’s administration running huge budget deficits in 1933.

泡沫破裂、市场经济下滑,必然引发重大政治变革、巨额赤字及大规模债务货币化。1927-1933 年案例中,1929-1932 年市场经济下滑,1932 年政治变革,进而导致罗斯福政府 1933 年出现巨额财政赤字。

His central bank printed a lot of money, which devalued money (e.g., in relation to gold). Devaluing money in this way alleviated the money shortage and a) helped the systemically important debtors that were being squeezed make debt service payments, b) raised asset prices, and c) stimulated the economy. Leaders who come to power in moments like this also typically make many shocking fiscal changes that I don’t have the space here to explain in detail, but I can say that these times generally lead to great conflicts and great transitions of wealth. In the Roosevelt case, these circumstances led to many big fiscal policy changes to shift wealth from the top to the rest (e.g., raising the top marginal income tax rate to 79% from 25% in the 1920s, raising estate and gift taxes sharply, and funding big increases in social programs and subsidies). It also led to great conflicts both within countries and between countries.

美联储大量印钞致货币贬值(如相对黄金),缓解货币短缺,同时:a)帮困境中的系统性重要债务人偿债;b)推高资产价格;c)刺激经济。此阶段上台的领导人通常还会推行激进财政变革,篇幅有限不细述,但此类时期易引发严重冲突与重大财富转移。罗斯福执政时,便推出多项财政政策,将财富从顶层向其他群体转移(如最高边际所得税率从 20 年代 25% 提至 79%,大幅加征遗产赠与税,增加社会福利补贴),也引发国内外严重冲突。

That is the classic dynamic. Throughout history, it has led too many leaders and too many central banks to name to do the same things too many times in too many countries over too many years for me to recount here. By the way, before 1913, the US didn’t have a central bank, and the ability of the government to print money didn’t exist, so bank defaults and deflationary depressions were more typical. In either case, bond holders do badly, and gold holders do well.

这是典型机制,历史上多国多年来,无数领导人和央行多次践行,不胜枚举。顺带一提,1913 年前美国无央行、政府无印钞权,银行违约与通缩性萧条更常见。无论哪种情况,债券持有者受损,黄金持有者受益。

But while the 1927-33 example is a good one of what the classic bubble-bust cycle looks like, that case is one of the more extreme ones. You can see the same dynamic in what led President Nixon and the Fed to do the exact same thing in 1971 and led virtually all the other bubbles and busts to happen (e.g., 1989-90 in Japan, the 2000 dot-com bubble, etc.). These bubbles and busts have a number of other typical characteristics (like the market being very popular with unsophisticated investors who are drawn in by the popularity, buy in a leveraged way, lose a lot of money, and get angry).

1927-1933 年案例虽能体现典型泡沫 - 崩盘周期,却较为极端。1971 年尼克松总统与美联储举措、1989-1990 年日本泡沫、2000 年互联网泡沫等,均是同一机制。这些泡沫与崩盘还有其他典型特征(如市场受普通投资者追捧,他们跟风杠杆买入,亏损后心生不满)。

This dynamic has worked this way for thousands of years when these conditions existed (i.e., when the demand for money became greater than the supply of it). Wealth had to be sold to get the money, bubbles popped, and defaults, money printing, and bad economic, social, and political things happened. In other words, that imbalance between the amount of financial wealth and money and the turning in of financial wealth (especially debt assets) for money is what has always caused runs in banks, both private banks and government-controlled central banks. These runs led either to defaults (which mostly happened prior to the creation of the Federal Reserve) or the creation of money and credit by the central bank to be given to those who were too important to be allowed to fail so that they could service their loans and not fail.

数千年来,只要货币需求大于供给,该机制就会生效:售富换钱、泡沫破裂,违约、印钞及各类负面事件发生。简言之,金融财富与货币失衡、金融财富(尤其债务资产)换钱,是私人银行与央行挤兑的根源,挤兑要么致违约(多在美联储成立前),要么央行造货币信贷救助关键机构。

So, keep in mind:

When the promises to deliver money (i.e., debt assets) are far greater than the amount of money that exists, and there is a need to sell financial assets to get money, watch out for a bubble bursting and be sure you’re protected (e.g., don’t have significant credit exposures and own some gold). If that happens when there are big wealth gaps, watch out for big political and wealth changes and be sure to be protected against them.

需牢记:当货币兑付承诺(即债务资产)远超现存货币,且需售金融资产换钱时,警惕泡沫破裂,做好防护(如规避大量信贷敞口、持有黄金);若此时有贫富鸿沟,警惕重大政治与财富变革,做好应对。

While interest rate increases and tightenings of credit have been the most common causes of the selling of assets to get the money that was needed, any reason that creates a need for money—for example, wealth taxes—and the selling of financial wealth to get that money could lead to that dynamic.

加息与信贷收紧是售资产换钱的常见原因,但任何致货币需求增加的因素(如财富税)及售富换钱行为,均可能触发该机制。

When there is a big wealth/money gap at the same time as there is a big wealth gap, that should be viewed as a very risky set of circumstances.

当财富与货币差距、贫富鸿沟同时扩大,属极高风险情形。

From the 1920s Until Now 从 20 世纪 20 年代至今

(You can skip this if you don’t care to read a quick description of how we got from the 1920s to now.)(若无意了解 20 世纪 20 年代至今发展脉络,可跳过)

While I touched on how the 1920s bubble led to the 1929-33 bust and depression, to quickly bring you up to date, that bust and the resulting depression led to President Roosevelt’s 1933 default on the US government’s promise to give the then hard money (gold) at the promised price. The government printed a lot of money, and gold rose by approximately 70%. I will skip going over how the 1933-38 reflation led to the 1938 tightening; how the “recession" of 1938-39 created the economic and leadership ingredients that, together with the geopolitical dynamic of the German and Japanese rising powers challenging the British and American leading powers, led to World War II; and how the classic Big Cycle dynamic took us from 1939 to 1945 (when the old monetary, political, and geopolitical orders broke down and the new ones were set up).

虽提及 20 年代泡沫致 1929-1933 年崩盘与大萧条,简要梳理现状:此次崩盘与大萧条让罗斯福 1933 年违背美国政府按承诺价兑换硬通货(黄金)的约定,政府大量印钞,黄金涨价约 70%。略过 1933-1938 年通胀回升致 1938 年收紧、1938-1939 年 “衰退” 叠加德日崛起挑战英美主导的地缘格局致二战、1939-1945 年旧秩序瓦解新秩序建立的大周期过程。

I won’t dive into why, but I will note that these things led to the US becoming very rich (it held two-thirds of the world’s money, which was then gold) and powerful (it produced half of world GDP and was the dominant military power). So, when the new monetary order was set out in the Bretton Woods agreement, it continued to base money on gold, the dollar was linked to gold (other countries could use the dollars they acquired to buy gold at $35 an ounce), and other countries’ currencies were linked to gold. Then, between 1944 and 1971, the US government spent a lot more than it took in from taxes, so it borrowed a lot, which it sold as debt, thus creating a lot more claims on gold than there was gold in the central bank. Seeing this, other countries started turning their paper money in for gold. This made money and credit undesirably tight, so President Nixon did the same thing in 1971 as President Roosevelt did in 1933, again devaluing fiat money relative to gold, and the price of gold soared. Suffice it to say that from then until now, a) government debt and debt service costs rose sharply relative to the tax income needed to service the government debt (especially in the 2008-12 period following the 2008 global financial crisis and since 2020, when there was the COVID financial crisis); b) income and values gaps grew to where they are now, which is very large, so we now have irreconcilable political differences; and c) the stock market is probably in a bubble boosted by the credit-, debt-, and creativity-supported speculations on new technologies.

不深究原因,但需指出:这些事件让美国极富(持全球三分之二黄金货币)且强(占全球 GDP 一半、军事主导)。布雷顿森林协议确立新货币秩序,仍以黄金为基础,美元挂钩黄金(他国可按 35 美元 / 盎司兑金),他国货币间接挂钩黄金。1944-1971 年,美国支出超税收,大量举债,黄金兑付需求超储备,他国纷纷兑金,货币信贷收紧,尼克松 1971 年效仿罗斯福让法定货币兑金贬值,黄金暴涨。简而言之,此后至今:a)政府债务及偿债成本相对税收大幅上升(尤其 2008 金融危机后 2008-2012 年、2020 年新冠金融危机后);b)收入与财富差距扩至当前极高水平,政治分歧难调和;c)信贷、债务及新技术投机推高股市,或处泡沫。

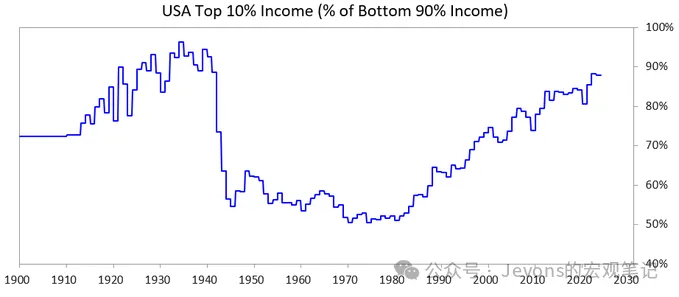

下图显示收入前 10% 与后 90% 群体占比,当前差距极大。

Where We Are Now 我们当前所处境地

The United States and all the other countries’ governments that have overborrowed and are democratically run are now in a position where they a) can’t increase their debts as they did before, b) can’t raise taxes enough, and c) can’t cut spending enough to prevent running deficits and increasing their debts. They are stuck.

美国及其他负债过高的民主国家政府,现陷入困境:a)难再像以往加债;b)难大幅增税;c)难大幅减支以避赤字与债务增加,进退两难。

To explain in more detail:

They can’t borrow enough because there isn’t adequate free-market demand for their debt. (This is because they are already overindebted, and the holders of their debt already have too much of it.) Also, international holders of debt assets of other countries (e.g., China) worry that the war-like conflicts could lead to them not being paid back, so their buying of bonds is waning and they are shifting their debt assets into gold.

具体而言:难充分举债,因市场对其债务需求不足(政府已负债过高,持有者持仓饱和);且他国债务持有者(如中国)担忧冲突致违约,购债意愿降,转持黄金。

They can’t raise taxes enough because if they raise taxes on the top 1-10% of people (who have most of the wealth), a) these people will leave, taking their tax paying with them, or b) the politicians will lose the support of the top 1-10% (which is important to fund expensive campaigns), or c) they will pop the bubble.

难大幅增税,因对财富集中的前 1%-10% 加税:a)他们或移民,带走税收;b)政客失其支持(关乎竞选资金);c)或刺破泡沫。

And they can’t cut spending and cut benefits enough because that’s politically and, perhaps, morally unacceptable, especially as those cuts will disproportionately affect those in the bottom 60%…

难大幅减支与福利,因政治、道德层面难接受,尤其减支对底层 60% 群体影响更大………

so they are stuck.故陷入僵局。

For these reasons, all democratic governments in countries that have big debt, big wealth, and big values differences are in trouble.

因此,负债高、财富差距大、价值观分歧大的民主国家政府均陷困境。

Given these conditions, the way the democratic political system works, and what people are like, politicians are promising quick fixes, failing to deliver satisfactory results, and are quickly being thrown out of office and replaced by new politicians who are promising quick fixes, failing, and being replaced, and so on. That’s why the UK and France, which have systems that can replace leaders quickly, have each had four prime ministers in the last five years.

在此背景下,结合民主政治运作与人性,政客承诺快速解决方案却难兑现,迅速下台,新政客上台重蹈覆辙,循环往复。这也是英、法这类易换领导人的国家,过去五年各换四位首相的原因。

Said differently, we are now seeing the classic pattern that is typical at this stage in the Big Cycle. This dynamic is very important to understand and should now be obvious.

换言之,我们正见证大周期此阶段的典型模式,该机制至关重要,如今显而易见。

同时,股市与财富繁荣集中于顶级 AI 相关股(如七大科技巨头)及少数富豪,AI 替代劳动力,既扩财富与货币差距,也加剧贫富鸿沟。基于历史经验,我认为极可能出现政治社会反弹,至少改变财富分配,极端或致社会政治动荡。

Let’s now look at how this dynamic and the big wealth gaps together are causing problems for monetary policy and could lead to wealth taxes that would prick the bubble and lead to a bust.

接下来看该机制与贫富鸿沟如何给货币政策施压,或催生财富税,进而刺破泡沫、引发崩盘。

What the Numbers Look Like 数据情况

I will now compare those in the top 10% of wealth and incomes with those in the bottom 60% of wealth and incomes. I picked the bottom 60% because that constitutes the majority of people.

现对比财富收入前 10% 与后 60% 群体,选后 60% 因占人口多数。

In brief:

The wealthiest (top 1-10%) have greatly more wealth, income, and stock ownership than most people (the bottom 60%).

Most of the wealth of those who are the wealthiest is coming from their wealth increasing in value, which is not taxed until the wealth is sold (which is different from income, which is taxed as it is earned).

With the AI boom, those gaps are increasing and likely to expand at an accelerating pace. If wealth is taxed, that will require asset sales to pay the taxes, which could pop the bubble.

简要概况:

最富裕群体(前 1%-10%)财富、收入、持股量远超后 60%;

其财富多来自资产增值,出售前不征税(与收入赚即征税不同);

AI 热潮下,差距持续扩大且或加速;

若征财富税,需售资产缴税,或刺破泡沫。

More specifically:In the US, the top 10% of households are the well-educated and highly economically productive people who earn about 50% of all income, have about two‐thirds of total wealth, hold about 90% of all equities, and pay about two-thirds of federal income taxes, with all of these numbers growing at a good pace. In other words, they are doing great and contributing a lot.

具体来看:美国前 10% 家庭多为高学历、高生产力群体,收入占总收入 50%,拥三分之二总财富,持 90% 股票,缴三分之二联邦所得税,且比例稳步上升,处境佳、贡献大。

In contrast, the bottom 60% are not well-educated (e.g., 60% of all Americans have below a sixth-grade reading level), relatively unproductive economically, and combined earn just about 30% of all income, own only 5% of all wealth, own only about 5% of all equities, and pay under 5% of all federal taxes. Their wealth and economic prospects are relatively stagnant, so they are squeezed financially.

反观后 60%,教育程度低(60% 美国人阅读水平低于六年级)、生产力弱,总收入占 30%,仅拥 5% 财富、5% 股票,缴不足 5% 联邦所得税,财富与经济前景停滞,财务承压。

Naturally, there is great pressure to tax and redistribute the wealth and money from those in the top 10% to those in the bottom 60%.

向顶层 10% 征税、向底层 60% 再分配的压力自然极大。

While we never had wealth taxes, there is now a lot of pressure to have them at both the state and federal level. Why tax wealth now when it wasn’t taxed before? Because that’s where the money is—i.e., because most of those at the top are getting richer through their wealth increases, which aren’t taxed, rather than through their earned income.

美国从未征过财富税,但如今州与联邦层面征税呼声高涨。为何如今征税?因财富集中于顶层,他们致富多靠免税的资产增值,而非劳动收入。

Wealth taxes have three big problems:

- The rich can move, and if they move, they take their talents, productivity, income, wealth, and tax paying with them, reducing them in the places they leave and boosting them in the places they go to;

- they are difficult to implement (for reasons you probably know and don’t want me to digress into because this note is already too long); and

- they take money away from the investments that finance the productivity-gaining activities to give it to the government under the unlikely assumption that they will handle it well to make those in the bottom 60% productive and prosperous.

财 富税存在三大问题:

- 富人可迁移,带走才能、生产力、收入、财富与税收,致迁出地受损、迁入地受益;

- 实施难度大(原因易懂,篇幅有限不赘述);

- 从生产力投资中抽钱给政府,且难保证政府能善用资金提升底层群体生产力与财富。

For these reasons, I would much prefer to see a tolerable tax (e.g., a 5-10% tax) on unrealized capital gains. But that’s another subject for another time.

因此,我更倾向对未实现资本利得征适度税(如 5%-10%),此为另一话题,留待日后探讨。

P.S. So How Would a Wealth Tax Work?

附言:财富税如何运作?

In a future note, I will address this issue more completely. Suffice it to say that the US household balance sheets show roughly $150 trillion of gross wealth, but less than $5 trillion is in cash or deposits. So, if a 1-2% annual wealth tax were imposed, the cash requirement would exceed $1-2 trillion per year—while the liquid cash pool is not much larger than that.

后续文章将详析此问题,简而言之,美国家庭总财富约 150 万亿美元,现金存款不足 5 万亿美元。若征 1%-2% 年度财富税,年现金需求超 1-2 万亿美元,与流动现金规模接近。

Anything like that would pop the bubble and lead to a bust. Of course, wealth taxes wouldn’t be levied on all people; they would be levied on the rich. I won’t get into the numbers now, as this piece has gone on long enough. Suffice it to say that wealth taxes would 1) trigger a forced selling of private and public equity, depressing valuations; 2) increase credit demand, potentially inflating borrowing costs for the wealthy and for markets generally; and 3) encourage offshoring or relocation of wealth to friendlier jurisdictions. These pressures become acute if governments impose wealth taxes on unrealized gains or illiquid assets such as private equity, venture holdings, or even concentrated public equity positions.

此类税收必刺破泡沫、引发崩盘。当然,财富税不针对全民,仅针对富人。不深入数据,因文章已过长。需说明,财富税将:1)触发公私股强制抛售,压低估值;2)增信贷需求,或推高富人及市场借贷成本;3)促使财富向税收友好地区转移。若对未实现收益或私募股权、风险投资等非流动资产征税,压力将剧增。

END

Jevons的宏观笔记